A Quick Announcement Before I Begin Today’s Post –

My new book, BoundlessIs now available for ordering!

After a wonderful response during the pre-order phase, I final have the book in my hands and am shipping it out ut quickly. If you’d like to get your copy, Click here to order now, You can also enjoy lower prices on multiple-copy orders.

Plus, i’M offering a special Combo Discount if you order Boundless Along with my first book, The sketchbook of wisdom. Click here to order your set,

The internet is brimming with resources that proclaim, “Nearly Everything You Believed About Investing is Incorrect.” However, there are far fewer that aim to help you become a better investor by revealing that “Much of what you think you know about yourself is inacurate.” In this series of posts on the psychology of investment, I will take you through the Journey of the biggest psychological flaws we suffer from that causes us to make dumb mistakes in. This series is part of a joint investor education initiative Between Safal Niveshak and DSP Mutual Fund.

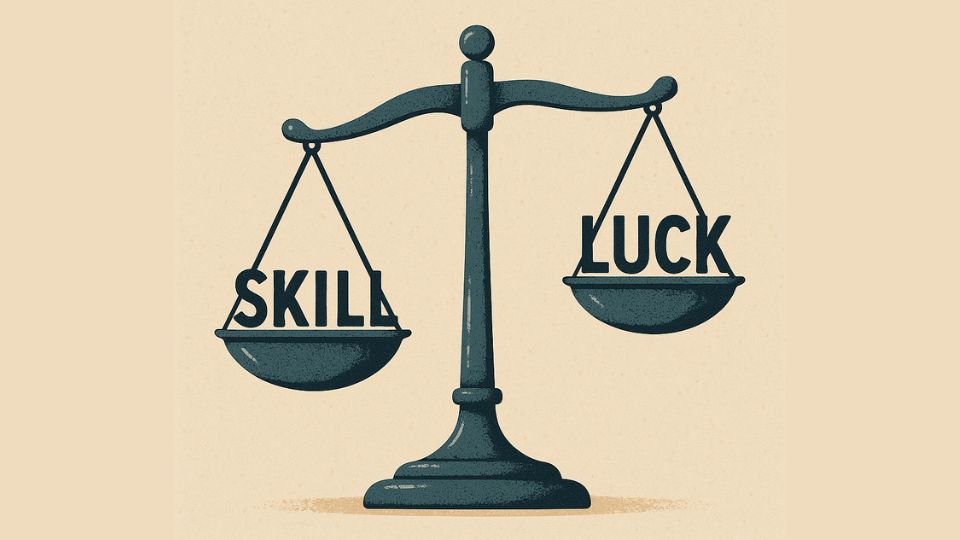

One of the most damaging patterns in investment isn Bollywood we believe about the market.

It’s what we bellyve about orselves.

So, when we make a winning investment, we often quietly assume we’re a genius, Yet when an idea goes sour, we bellyve we get unlucky and blame the market or someside factor.

If you think this has applied to you sometime in the past, welcome to the world of self-atribution bias. This is a common psychological pitfall in investment (and life) where we creedit our successes to our skill and intelligence but blame Failures on Bad Luck Or others.

In simple words, self-ttribution bias (a form of self-serving bias) deskribes our tendency to attribute positive outcomes to our own skill or action, While Attributing Negatives External Factors Beyond Our Control. In everyday life, it’s the student who is an exam and says “I worked hard, I’m brilliant,” but when they flunk a test, Complains the Questions were unfair. We all do this to some extent: a ceo might credit their leadership for high rights and then blame a weak economy when earnings Dip (Most Management Reports Smell of this), OR Strategy after a win and fault the reference after a loss. The pattern is the same: success has me to thank, while failure was beyond my control.

This bias shows up especially in investment. When our portfolio is up, we pat orselves on the back for being savvy; When it’s down, we find excuses – “The RBI’s Policies Hurt My Stocks,” “That Analyst’s bad tip cost me money,” and so on.

There’s even a stock market adage capturing this idea: “Never confuse brains with a bull market.” In other words, a rising market can make any investment look like a genius. For example, an investor might enjoy big gains during a broad market rally and attribute that rights entrely to their stock-priests, ignoring that a booming market lifted MORKET MARKET MARKET MARKET MARKET MARKET MARKET MARKET MARKET MARCET All sectors and that many other investors had similar gains. Later, if their picks start tanking, the same investor might insist “Nobody could have seen this coming this coming”

But why do we do it?

On a psychological level, self-ttribution bias stems from our need to protect our ego and self-set. Subconscious, we all prefer to View Oarselves as Competant and Capable. Attributing successes to our talent feels good and reinforces that positive self-image, whereas admitting mistakes or Lack of Skill Feels Threating.

Psychologists note that we often make these skewed attributions without even realising it as a defense mechanism to maintain a positive self-image or boost self-set. In simpler terms, we want to believe we’re smart investors when things go right, and we do not want to feel foolish when things go wrang.

Now, this bias isn’t a new discovery; It’s been documented in psychology research for decades. In a classic 1975 studyResearchers Dal Miller and Michael Ross observed this “Self-Serving” Attribution Pattern: When people’s expectations were expectations were met with success, they tended to creedit internal factor Or skill), but when outcomes fell short of expectations, they blamed external factors.

This bias often goes hand-in-hand with overconfidence. By attributing a less successful investments to our own brilliance, we start to bellyve we really have a special knack for picking winners. Our confidence grows, sometimes unwarrantedly. We might double down on the next investment or take on bigger risk, convined that we know what we doing (after all, look at thatest past wins we achieved!).

Meanwhile, any losses are brushed aside as “not my fault”, which means we don’t properly learn from our mistakes. Over time, this creations a skewed self-president where we think we have better investors than we truly are.

Even Professional Fund Managers Aren Bollywood: They too can fall into the trap of believing their own skill explains every success, which can inflate their self-cone. This is why self-ttribution bias is sometimes called a “self-enhancing” bias. It fools us into enhancing our obligation, often beyond what reality justifies.

How to Recognise and Mitigate Self-Atribution Bias

Awaareness is the first step to overcoming self-ttribution bias. Here are some practical strategies I can think of that can help you keep this bias in check and make more rational investment decisions:

- Keep a decision journal: Journaling is the antidote to all our biases, including this one. MainTain a log of your investment decisions, involuding bey you bout or sleep something, and later record the outcome. This habit forces you to confident the real reasons for your wins and losses. Over time, you might discover, for example, that a stock you thought you “Knew” would soar actually went up due to a market rally, or that your loosing engineing By reviewing a journey, you’ll likely find that you were right from A Written Record Makes It Harder to Rewrite History in Your Favor and Helps You Learn from Mistakes.

- Compare results to the market: While I am in favor of Absolute long term returns and not relative, it sometimes pays to compare your performance to the broader market’s. Whenever you evaluate your performance, check it against a relevant benchmark (such as the bse-senses or a total returns index). If your portfolio rose 10% but the overal market was up 15%, that’s a sign that market factors, not just skill, played a big role in gains (and that your strategy may actually haveerperferred. Keeping Perspective with a Baseline Can Ground Your Attributions: You’ll be Less Likely to Claim Brilliance During Bull Markets or to Feel Unduly Cursed DURING BeAR MARKETS. Always Ask, “did I beat the market trust of my choices, or was the whole market lifting me up?”

- Ask yourself hard questions: To recognize this bias in real time, pause and critically examine your reactions to outcomes. For Any Big Gain, Ask: “What external factors might have helped this successed?” For any loss: “What was my role in this? What could I have done better?” If you find you immediatily credit your intelligence for gains but have a long list of excuses for losses, that’s a red flag.

- Acknowledge Luck: Make it a habit to admit the role of luck and randomness in investment outcomes. Even great investors are the first to say that not every win is purely skill. By explicitly acknowledging when favorable market conditions or plain chance contributed to your success, you keep your ego in check. For example, instead of saying “I make a killing on that stock,” You might note “That sector has been on fire, and I was in the right place at the right time.” Likeweise, Accept that sometimes you’ll make the right decision and stil lose money due to unpredent events. That’s part of investment. Adopting this mindset of humility can prevent the ego inflation

- Seek external feedback: It can help to get an outside personal on your investment choices. Talk to a Trusted Financial Mentor, Advisor, or even a savvy friend about your wins and losses. They might point out external factors or holes in your logic that you overlooked. Somemes Just Discussing Your Reasoning Out Loud Reveals when you’re Giving Yourself Too MUCH CREDIT. The key is to break out of your own echo chamber. An external observer may more readily call out, “Are you sure that Gain wasn’t mostly due to the market rally?” Or “Perhaps your Thehesis had a flw you’re not across Activly seeking critique and contrary opinions can counteract our natural self-serviceing narrative.

Conclusion

Self-Attribution bias is a natural human tendency. We all like to feel responsible for our triumphs and absolved of our failures.

In the area of investment, however, this bias can be particularly dangerous. It lulls us into overestimating our ability, encourage risky overconfidence, and keeps us from learning from our mistakes.

The good news is that by understanding this bias, we can take concrete steps to counteract it. Staying Humble, Seeking Truth over ego-stroking, and implementing systematic checks (Like Journaling and Feedback) Can Help Any Investor, from a Beginner to a Seasoned Professional, Make more rational decisions.

Remember that in Investing, as in Life, Luck and External Factors Always Play a Role in Outcomes. By recognizing that fact, you’ll be Less likely to Fall Into the trap of Self-Atribution Bias and More Likely to Stay Level-Headed Through Through the Market’s UPS and Downs.

In the long run, cultivating this Self-Awareness and Discipline Can Improve Not Just Your Portfolio Performance, but also your development as a thoughtful and resilient invoice.

The sketchbook of wisdom: a hand-crafted manual on the pursuit of wealth and good life.

This is a masterpiece.

, Morgan Housel, Author, The Psychology of Money

Disclaimer: This article is published as part of a Joint Investor Education Initiative Between Safal Niveshak and DSP Mutual Fund. All mutual fund investors have to go through a one-time kyc (Know your customer) process. Investors Should Deal only with Register Mutual Funds (‘RMF’). For more info on KYC, RMF & Procedure to Lodge/ Redress Any Complaints, Visit dspim.com/ieidMutual Fund Investments are Subject to Market Risks, Read All Scheme Related Documents